What is power?

Not in the context of superheroes or physics, but in the social context – what makes a person or a group of people powerful? Those who can manifest their will into reality, like making other people do or give what they want, are considered powerful. Well… how does one compel others? Leverage – specifically, relative bargaining power (RBP). In almost all instances, the party that gets the favorable end of a deal has greater bargaining power relative to their counterparty. It determines everything from the price of housing to who gets the better end of a trade deal, all the way to how resources are distributed within society.

An astute reader might notice that this thesis aligns closely with the study of cooperative bargaining and the Nash Bargaining Solution in game theory, which assert that relative bargaining power determines the distribution of surplus in any mutual transaction between two parties. My value-add in this article comes from the application of this theory at a grander, practical scale rather than purely theoretics.

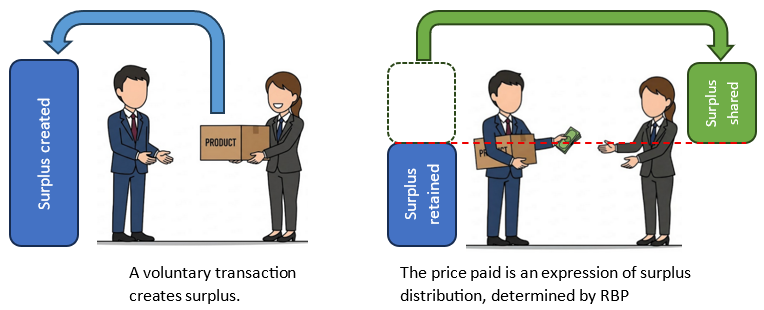

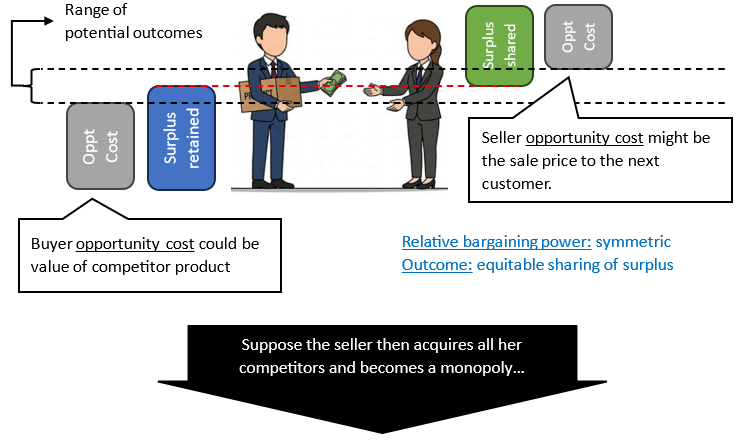

In simpler terms, when two parties voluntarily engage in an exchange, value (aka surplus) is created, otherwise they wouldn’t do it. Relative bargaining power overwhelmingly determines how that surplus is distributed among parties in an economic relationship. Price is the most common expression of relative bargaining power – it is the return of some of the surplus that the transaction created back to the seller. When the price paid is high, the seller has higher relative bargaining power than the buyer.

False perception, stupidity, or madness can also result in favorable outcomes…

Some minor exceptions to RBP exist, like false perception, stupidity, and madness. Ultimately, it’s perceived bargaining power that really matters, and if one party misleads the counterparty into overestimating one’s bargaining power (i.e. bluffing), it could result in a more favorable outcome. Additionally, insanity or stupidity (real or feigned) could supersede bargaining power, think: President Nixon’s madman theory. Ultimately, none of these strategies work in the long-run or in repeatable negotiations, where the truth reconciles with false perceptions. The scope of this article is to discuss long-term outcomes, so we’re not here to explore poker strategies.

There is only one exception that can supersede RBP in the long-run: sovereignty.

I contend that RBP is the sole determinant of SURPLUS distribution in any given system over the long-run (surplus refers to the total “utility” created by a given exchange for a certain category of product or service exchanged). RBP is the source of power for the elites throughout history, and they constantly seek more ways to increase their RBP and thereby extraction of surplus from direct and indirect counterparties. The issue with oligarchs is that they leverage existing bargaining power to compound itself over time, extracting more and more surplus from the system until it devolves into feudalism. Conventional economic theory thoroughly fails to understand RBP at a high level, which results in some ridiculous policy prescriptions from liberal capitalist institutions. I will discuss these flaws in Part 1.2.

Definition of relative bargaining power

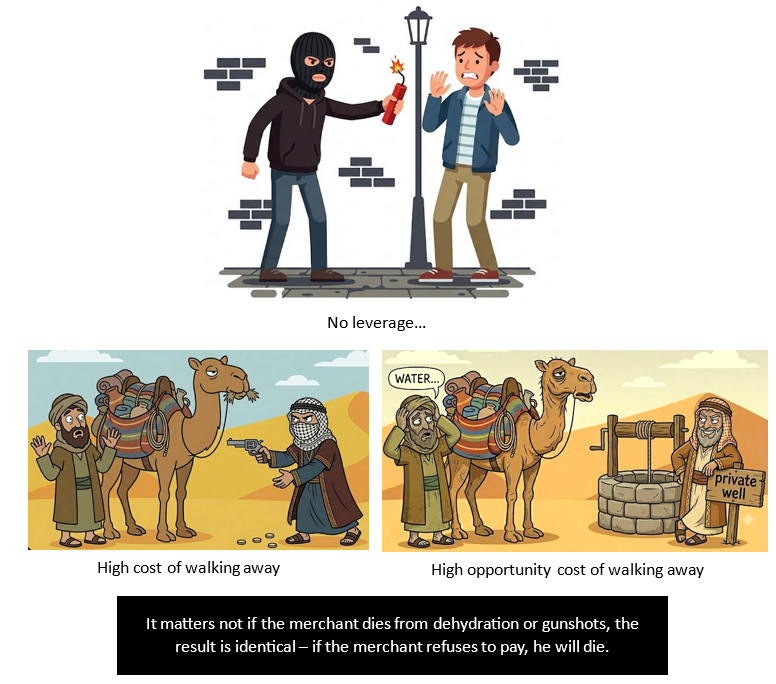

Digging deeper, what even is RBP? Bargaining power is only useful in the context of social interactions – someone having bargaining power over nobody makes no sense; this is why we specify “relative” bargaining power. In negotiations, “walking away” is a power move; the party most willing to walk away (without bluffing) from the deal has higher bargaining power. What determines the willingness to walk away? The ability of the counterparty to impose costs for walking away, including opportunity cost. However, if imposing that cost on the counterparty also costs oneself significantly, then that’s not real bargaining power either – it is like trying to rob someone with a stick of dynamite. Imposed cost must be asymmetric. Therefore, bargaining power is the ability to impose asymmetric costs or opportunity costs on the counterparty for walking away.1 Relative bargaining power is the comparison of which party has the greater ability to inflict asymmetric cost on the other for walking away. They say that walking away in the middle of negotiation is a power move – it demonstrates precisely this principle, that one side was unable to impose sufficient cost to prevent the other from walking away.

1956 Suez Crisis

When Israel, France, and Great Britain invaded Egypt to protect their imperial interests, they were met with a stark reality. The three nations had conspired to topple Nasser’s government and replace it with a pliant puppet. Although laughable today, back then, France and Great Britain desperately clung onto their delusions of grandeur, believing they still possessed the imperial power they once held.

Although the military invasion succeeded, the entire ordeal became a political disaster for the British and the French, who were thoroughly humiliated. The United States under President Eisenhower threatened to dump British government bonds, blocked the British from accessing IMF loans, and refused to ship them oil (Nasser had sabotaged the Suez Canal to block oil shipments). The Soviets under Khrushchev threatened all three invaders with dramatic escalation, a combination of a nuclear threat and indirect military intervention through Syria. Thus, the British, French, and Israelis were forced to withdraw from Egypt.

This event clearly delineated the end of Britain and France as global superpowers and affirmed the ascendancy of the United States and the USSR in their places. It became clear to all who really wielded power, i.e. the leverage to compel another party to comply without war.

Relative bargaining power determines surplus distribution

To begin the analysis of RBP and how it determines surplus distribution, we must define “baseline.” Recall in my prior article that reproductive subsistence is the bare minimum level (i.e. baseline) of resources required to survive and reproduce at a maintenance level, ensuring a stable population. In the context of RBP, baseline means the minimum amount of concessions or value provided to one party in the deal to ensure the counterparty would not walk away. Any value created above baseline is called “surplus.”

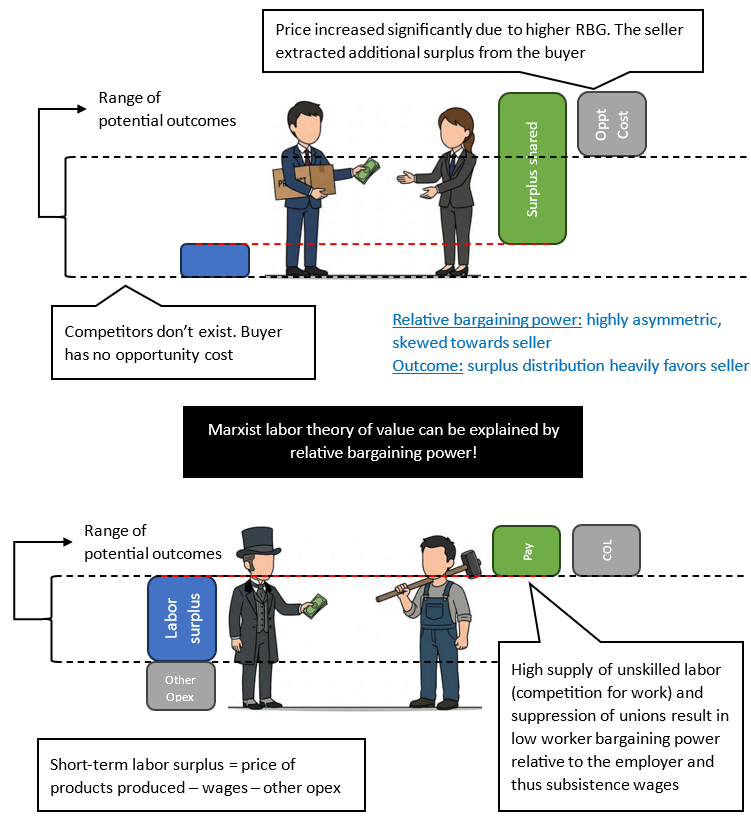

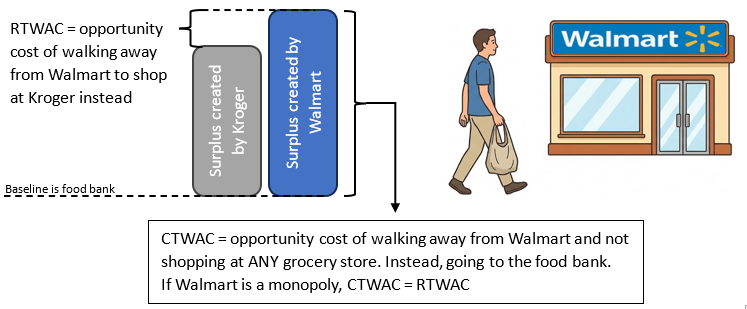

We must examine the cost of walking away on a “whole-category basis.” In other words, the alternative to the deal not happening with a vendor – it isn’t to simply do the deal with a competitor – it’s to not do ANY deal with ANY vendor of that category. In that sense, the alternative to walking away from a supermarket and not buying food would be to go to the food bank, not to just go to another supermarket (because competition is a source of bargaining power, accounted for later, when determining surplus distribution). The category total walking away cost (CTWAC) is equal to the cost and opportunity cost from not doing ANY deal with ANY counterparty in a particular category. In contrast, the real total walking away cost (RTWAC) would be equal to the cost of walking away from just that one counterparty, accounting for ALL alternatives. In other words, a party’s CTWAC should generally be much higher than RTWAC, but as their options (e.g. competitor products) dwindle, their RTWAC approaches CTWAC. Therefore, a vendor that buys up all their competitors technically “creates” more value for customers since RTWAC has increased to become RTWAC; the vendor can then increase prices commensurately to “share” in that “value creation.”

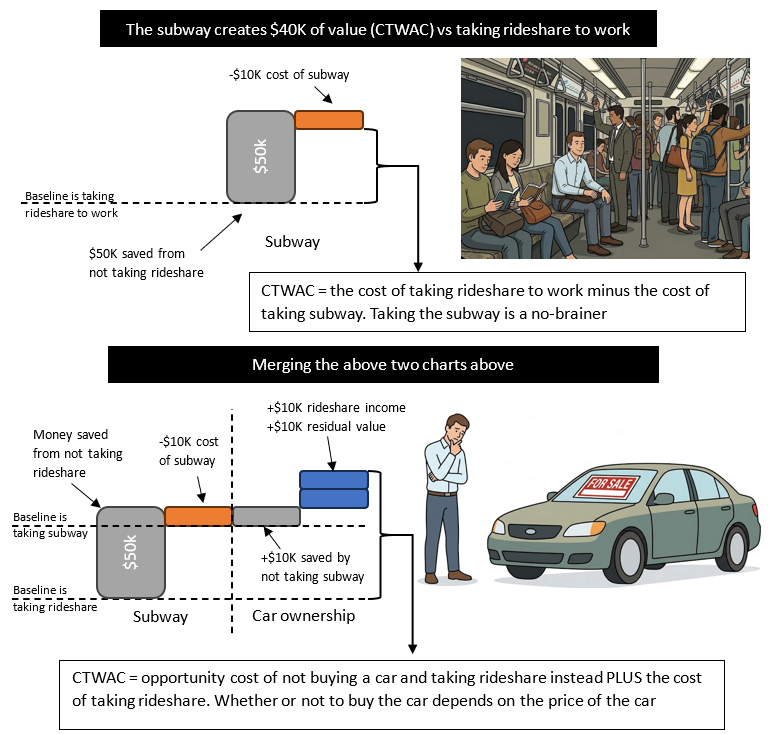

Car vs Rideshare Example

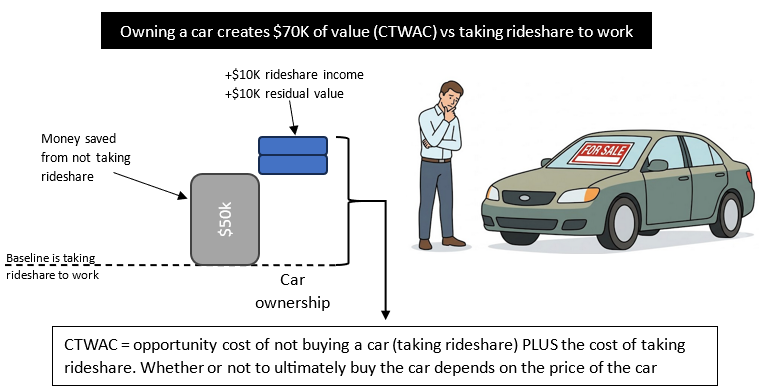

Let’s illustrate this with an example, ignoring time value of money and taxes for simplicity’s sake. Suppose there’s a man in the market for a car. He doesn’t own one currently and is about to start a job that requires commuting. There are no public transportation options in his city, so the only transportation options are either car ownership or rideshare. Assume the job pays $100K per year, with an expected tenure of 5 years ($500K total compensation over tenure).

- Suppose taking rideshare to work costs $50K over 5 years (cost for not buying a car)

- Additionally, if he buys the car, he can also do a bit of ridesharing himself in his free time, earning $10K over 5 years (opportunity cost for not buying a car)

- Lastly, the car would still have $10K of residual value at the end of 5 years (opportunity cost for not buying a car)

Therefore, if the man walks away from buying a car and thus opts to take rideshare, he has to pay $50K for rideshare and misses out on $20K of value from doing rideshare himself and the residual value of the car after 5 years. That gets us to the Category Total Walking Away Cost (CTWAC) of $70K.

Categories

Here, we’re defining the category as “car ownership,” which precludes ridesharing. If we broaden the category to include ALL forms of transportation (which determines whether the man can take the job at all), then the CTWAC for car ownership would be the opportunity cost of the income from the job, or $500K over 5 years, plus the $10K in rideshare income and $10K in residual value, for a total CTWAC of $520K. The CTWAC of taking rideshare to work would be $450K ($500K - $50K). If, for some reason, rideshare were the only way to get around the city and an oligopoly/monopoly, it could price FAR higher to extract a significant portion of that $450K in buyer surplus. That way, rideshare could effectively hold the economy hostage.

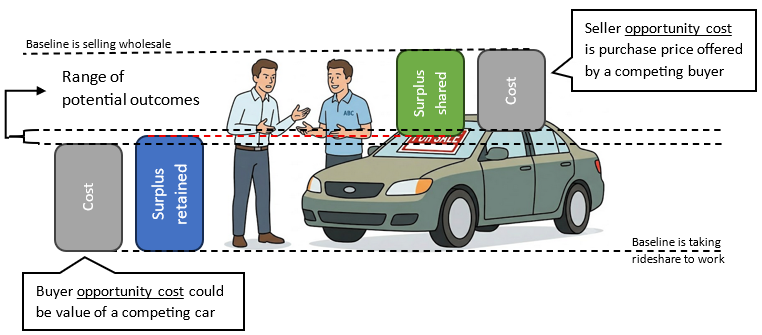

Suppose there’s an existing car manufacturer ABC selling directly to consumers, typically at ~$30K each. Assume ABC can easily sell their cars in the wholesale market at $25K (e.g. selling to rental companies, dealerships, etc.). For the car maker, their CTWAC for a deal with the man (the category is “retail car sales”) would be $25K of opportunity cost – this is effectively “subsistence” pricing. (If there were another buyer in the dealership that offered $30K to buy that car immediately, then the RTWAC for ABC is $30K).

Therefore, if the man buys the car from ABC at $30K, he achieves $40K of buyer surplus (CTWAC = $70K – $30K) vs taking rideshare to work, and ABC achieves $5K of seller surplus (CTWAC = $30K – $25K). If the man doesn’t buy from ABC, he can easily buy a different car from a competitor for say $32K. On the other hand, if ABC doesn’t sell to this particular man, they can easily sell to another customer for $30K. Therefore, the range of possible surplus distribution for car ownership is between $40K/$5K and $38K/$7K for the buyer and seller, respectively. Surplus distribution heavily favors the buyer, because car markets generally are highly competitive at the retail/dealership level.

Now… suppose the government starts restricting car imports, such that there’s less competition in the market. Additionally, the remaining car makers consolidate through M&A, such that there are far fewer competitors than previously. Due to less competition in the market, car makers have more bargaining power, since they can impose a higher RTWAC on the buyer and capitalize on that with higher pricing. Thus, declining competition results in higher pricing and extraction of consumer surplus.2 If rideshare didn’t exist and there’s an oligopoly in car makers, then those car makers would effectively gatekeep economic activity in this city.

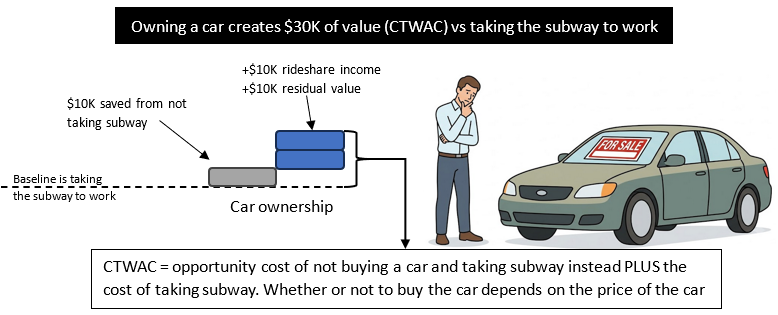

Then, let’s suppose the city government funds and builds an extensive network of subway in the area, such that it would only cost the man $10K over 5 years to get to work. Suddenly, the CTWAC for car ownership was reduced from $70K with ride sharing to $30K with public transportation (CTWAC vs subway as baseline = $10K cost of subway + $10K opportunity cost of ridesharing income + $10K opportunity cost of residual value of the car). The subway has massively increased the man’s RBP relative to car makers, such that it is now impossible for any car maker to charge more than $30K for selling the car to the man. Other people living in that same city likely experienced a similar reduction to CTWAC, so citywide car prices will decline as demand declines.

Don’t believe this is how the elites think? Please see Peter Thiel’s lecture at Stanford – it’s the most “mask-off” lecture I’ve ever seen, all about capturing surplus value from the perspective of a startup. For mature industries, it’s all about increasing RBP to capture surplus value that counterparties already enjoy. Startups and disruptors initially create great customer surplus, and once they become the incumbent and go IPO, it will be surplus extraction time, flexing their newfound RBP advantage over their customers. Prices will rise and the quality of goods & services will decline; this is textbook “enshittification.”

Diamond-water paradox

Recall that Adam Smith famously proposed the diamond-water paradox, where it seemed counterintuitive that water, an essential component of life, costs way less than diamonds, a mostly useless (at the time) rock.

Conventional economics today (neoclassical economics) explains this paradox by focusing on marginalism, which is the marginal utility of an extra liter of water versus the marginal utility of an extra diamond. The total utility of all water on earth is infinite, because without it, life would perish, but that’s not the scope of the negotiation. The utility of an extra liter of water is low because water is already plentiful. In contrast, diamonds are scarce (in theory), so the value of an extra diamond is very high. The next diamond is more in-demand than the next liter of water. At the core of it, price is based on supply and demand.

In Marxist Labor Theory of Value, water is valued less because it is very easy to collect under normal circumstances, whereas diamonds are expensive because it is difficult to find, extract, and refine. It is based on the amount of labor input to produce the product or service.

Both these theories fail to consider RBP between those who buy water and those who control the supply, ignoring the vital social context without which price could not exist! Recall that price is inherently social, as it cannot exist without at least two transacting parties. In any competent country with a serious government, the state invests in and tightly regulates water infrastructure, ensuring that clean water remains plentiful, easily accessible, and cheap for all. Any party that tries to monopolize water would find themselves competing against public water infrastructure, inhibiting surplus extraction. However, if there were true, unrestricted private monopoly ownership of water infrastructure (comparable to private ownership of an oasis in the desert), water prices would be exorbitantly high, due to bargaining power. It is no wonder that Sharia law, which deeply reflects the material conditions of pre-modern Arab people, codified that water is for everyone and must not be hoarded or monopolized at the expense of others; priority must be placed on the essential uses of water (i.e. drinking for people and livestock).

In contrast, ~80-90% of natural diamond distribution had been controlled by a single company – De Beers Group, founded by Cecil Rhodes. Without diving into the specifics of the tactics they used to maintain their monopoly control or their spectacular marketing campaigns, De Beer’s ability to command a high price for their diamonds was a function of their leverage over downstream buyers. A jeweler could hardly afford to refuse De Beers diamonds, and neither could would-be grooms.

Equilibrium surplus distribution

For a given level of RBP between two negotiating parties, equilibrium surplus distribution is the point at which current surplus distribution equals sustainable (long-term) surplus distribution. In other words, neither party can demand meaningful concessions from their counterparty without the deal falling apart long-term. In microeconomics, this is equivalent to the “kink” point, where increasing the price (concession from the buyer) results in elastic demand, whereas reducing the price (concession from the seller) results in inelastic demand.

For any given RBP between two negotiating parties, there’s an equilibrium surplus distribution. For example, under feudalism, the lord/serf distribution is 100%/0%. If current distribution is anything less than 100%/0%, then the lord can increase rent (extraction) without issue. If the current distribution is anything more than 100%/0% (like 110%/-10%), then the serf can win concessions (otherwise they die and the lord loses earnings power over time or the serf revolts, as they have nothing to lose). However, if the current surplus distribution is 60%/40%, and the equilibrium surplus distribution is 70%/30%, then the stronger party has ability to demand more concessions from their counterparty, approaching equilibrium over time. In business, this is called “pricing power.” There might be very good reasons why current surplus distribution ≠ equilibrium surplus distribution; for example, if the monopolist tries to price to equilibrium too quickly, they might attract unwanted regulatory scrutiny.

Example 1: Credit Rating Agencies

The corporate credit rating industry is an oligopoly among the big 3: S&P, Moody’s, and Fitch (though it’s mostly a duopoly between the first two). When a company issues debt, they typically can get it rated, the corporate equivalent of a credit score. However, the rating depends not only on the issuer but on the terms of the debt, so each debt security has its own rating. I’m simplifying the following details for brevity.

Since the advent of corporate credit ratings, the global financial markets have built itself around credit ratings; regulators, asset managers, insurers, banks, indices, etc. heavily rely on credit ratings for risk assessment, portfolio management, analysis, etc. To not have a rating increases the perceived risk and reduces liquidity/demand on the debt (many investors can only hold a tiny amount of unrated debt or none at all), which increase the interest rate that the borrower has to pay. All else equal, having two ratings reduce interest rate by about 50 basis points (0.50%). Why two? Because all the buyers require it – having at least two avoids being seen as having shopped around for the best rating.

Therefore, the total surplus in a ratings transaction is ~50bps (the cost of credit rating issuance is nearly $0 and it requires almost no capital to operate the business), and negotiations between the issuer and each ratings agency will determine how the 50bps are allocated. Obviously, the combined cost of the 2 ratings cannot exceed 50bps, since the issuer will just walk. Currently, ratings cost around 8bps each. Therefore, the surplus distribution between the 2 ratings agencies and the issuer is 16/34 or 32%/68%, which suggests the issuer has substantial bargaining power over the ratings agencies. But this is clearly not true, as the rating agencies have increased pricing consistently over time (from ~4bps in 2006 to ~8bps in 2025, according to Raymond James Research). The rating agencies can impose a cost of 50bps to the issuer for walking away from the deal, whereas the issuer can impose only a small amount of forgone revenue to the rating agencies for walking away from the deal – there are a lot more debt issuers than rating agencies. It’s obvious that the rating agencies have very high RBP vs the issuer.

Note that there is a small amount of competition within the industry, so large corporate borrowers who regularly issue new debt can demand price concessions based on volume discounts; the managers at the credit rating agencies would hate losing a large customer. Moreover, their financial strength reduces their cost for foregoing ratings (probably closer to 30bps instead of 50bps), since liquidity should still be strong for blue-chip issuers even without a credit rating. They can also negotiate private placement debt to circumvent the need for a credit rating altogether. Coca-Cola, for example, can probably demand 4bps or lower cost per rating.

For the broader market, the rating agencies cannot immediately price to just short of 25bps each rating for 100/0 surplus distribution because there’s still a bit of competition among the big 3. More importantly, if all 3 collude to hit maximum pricing immediately, that aggressive behavior would instantly trigger regulatory crackdown and antitrust intervention.

Example 2: FICO and the credit bureaus

Funny enough, pushing pricing too hard is precisely what’s gotten the consumer-equivalent of credit ratings into trouble recently… For context, FICO is basically a scoring algorithm with comically high 88% operating margins. The 3 credit bureaus, Experian, Equifax, and TransUnion are also an oligopoly that feeds data into FICO. Every time a large consumer credit transaction occurs (e.g. buying a house with mortgage, a car loan, etc.), FICO and the credit agencies get paid. They charge a de minimis amount compared to the total cost of the transaction but are indispensable for the financial infrastructure of the entire ordeal, since consumer debt is typically repackaged, securitized, and sold into the financial markets – scores are non-negotiable for the system. A consumer loan originator (e.g. mortgage banker) would be unable to sell the loan into the securities market without credit reports and/or FICO score, so they have no choice but to pay FICO and the credit bureaus their fees – their entire business model depends on it.

Historically, FICO had charged ~$0.60 per score, but starting in 2023, the company started aggressively hiking prices to almost $5 in 2025, hitting $10 in 2026! The credit bureaus have followed suit with their own massive price hikes (40-50% increase in 2026). All of these costs have been passed directly to consumers. Hilariously enough, the competitor to FICO (still have yet to crack FICO’s monopoly, since they’re just a marginal competitor) is VantageScore, which is run by a joint venture among the 3 credit bureaus, tried to portray itself as the “good guy” and FICO as the “bad guy” when they too hiked pricing aggressively, riding on FICO’s coattails. Their 2026 pricing is $4.00 through TransUnion, $4.50 through Equifax, and “free” through Experian’s premium data bundle (the extra price is baked into the premium fee!).

All these companies have overwhelming bargaining power, which they leveraged to push surplus distribution towards equilibrium. However, they did it way too quickly, which resulted in industry backlash and regulator attention. Trump’s Director of FHFA has now focused on these 4 companies for anti-competitive behavior and intends to potentially take aggressive regulatory actions. Will Director Pulte succeed? I’m skeptical.

Highly asymmetrical RBP illustrated

As I asserted at the beginning of the article, relative bargaining power is the sole determinant of long-term distribution of surplus within a system (with only a single exception). Before I get into the mechanics of how it works, it would be easier to illustrate it with an example.

Suppose there’s an island country, where:

- The vast majority of the land is owned by a small group of landed gentry, having carved up the island into large estates

- The principal economy is plantation slavery, where a cash crop is grown

- Order on the plantation is enforced by armed overseers

- There is no import market for slaves, so the gentry must keep their slaves at least at reproductive subsistence (see prior article)

- The average slave can produce $100 worth of cash crops annually, $70 of which is needed to keep him/her at reproductive subsistence

- The country has minimal infrastructure beyond some basic irrigation and roads leading to the main port city, which is also the capital

It’s self-evident that the gentry has maximum bargaining power relative to the slaves via the threat of force. The only thing that could worsen slave conditions would be if the island had a slave import market, such that the gentry could literally work their slaves to death without batting an eye, since slaves could be easily replaced, cheaper than it costs to keep them alive past a certain age (this was exactly the case on the Caribbean and Brazilian sugar plantations). But in that scenario, there’s no longer any negotiations, since the enslaved have absolutely 0 recourse against the gentry – there’s nothing to negotiate. However, for our scenario, the slaves have downside protection – the gentry cannot afford to extract so much profits such that their slave population declines (cannot extract more than the surplus in the system), threatening the sustainability of the entire system.

What is the average gross profit (GP) per slave for the gentry?

The answer is $30. I suspect it didn’t even occur to the reader that part of the $30 after subsistence costs could be spent on making the slaves’ lives a bit easier. That’s because slaveowners have simply no incentive to do so. They will extract the entirety of the surplus within the system.

Suppose the price of the cash crop increased 20% permanently, what is the GP per slave?

The answer is $50. The entire windfall surplus is captured by the gentry – the slaves’ lives haven’t improved in the slightest. Once again, this is because slaves have de minimis bargaining power relative to the gentry. The overseer also would see no benefit from the windfall, as they have little bargaining power compared to their bosses. The overseers are replaceable. The overseer presumably has at least some alternative opportunities, so they could demand a slight surplus.

Reality is never so neat and tidy as our hypothetical, just as how friction exists despite the physics professor’s deepest wishes. It is possible the real answer might be slightly higher than $50, at least for the short-run. The gentry might tell their overseers to work the slaves harder and eat into their reproductive surplus to capitalize on what they might think of as short-term opportunity. This level of extraction cannot be sustained, because the slave population would decline over time. Thus, GP per slave cannot be sustainably higher than $50, which is the labor surplus per slave.

Reverting to the original scenario, then suppose the price of the cash crop declines by 20%, what is the GP per slave?

The answer is $10, because the surplus has declined from $30 ($100 – $70) to $10 ($80 – $70), and the gentry captures all surplus. The entire shortfall is eaten by the gentry, because if they attempt to shift some of that shortfall onto the slaves, the population of slaves would decline over time. Again, the gentry cannot sustainably cut slave resource consumption to less than needed for reproductive subsistence over the long-run. However, the overseer’s pay likely gets cut – they have less downside protection than the slaves, since they were living modestly above subsistence (some surplus), i.e. they can actually save some money, since room and board were provided by the gentry.

Structural changes?

A naïve observer may say, “clearly, the institution of slavery is the problem. Let’s suppose by some miracle, the government emancipates all slaves in the country.”

This wouldn’t happen in the first place, since whatever government holds power would be beholden to the powerful plantation gentry, who control most of the country’s economy. Since the slaves have no surplus to be taxed, the gentry ultimately funds the government and its administrators. Correspondingly, the plantation owners hold too much bargaining power over the politics of the country. There is no scenario in which they would allow emancipation willingly and peacefully. But for our scenario, let’s just say that a more powerful neighboring country for whatever reason, by gunboat diplomacy, forced the government to abolish slavery.

Slavery immediately turns into feudalism. The freemen are now serfs, and their living conditions hardly improve.

Recall that the gentry still controls the overwhelming majority of land and thus possesses overwhelming bargaining power over the freemen. The freemen have nowhere to go and no means of feeding themselves – the gentry have captured a key resource: land and thus can gatekeep the means of making a living. There simply aren’t enough economic opportunities outside of working on the plantation – the work that the slaves previously did still need be done. If any freeman refuses to work on the plantation again, they would starve – any individual freeman has very little relative bargaining power compared to the gentry. Nor did the gentry need to compete for laborers, since the total number of workers didn’t change due to emancipation, neither did the amount of work available.

In fact, the freemen have nothing to offer except their labor – the gentry not only owned the land, but also owned/controlled the tools, the housing, the transportation of the crops to market, as well as the inbound transportation of necessities like food, medicine, and farming supplies into the plantations. All of those are vital to the operations of the plantation, thus the gentry retained overwhelming bargaining power relative to the freemen. The result is wholly predictable – the freemen are once more reduced to reproductive subsistence. If the freeman could produce $100 worth of cash crop like previously and on average costs $70 to keep at reproductive subsistence, then the gentry would continue to extract $30 of profit from the freemen through various means. The exact method of surplus extraction matters not – only relative bargaining power.

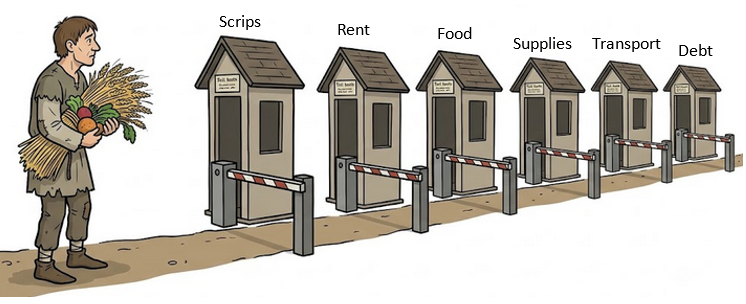

Just to illustrate my point, here are some of the options the gentry can employ to extract surplus from the freeman farmers on their land:

- Sharecropping (rent paid in share of crop)

- Price paid for crop, if not sharecropping (way below market price)

- Paid in fake money only usable at the plantation store (scrips)

- Price of supplies like food, medicine, farming supplies

- Rent of tools

- Fee for transporting the crops to port

- Debt peonage

Notice that the gentry controls both the cost of living (by setting prices for rent, food, supplies, etc.) and the revenue (by setting the price that the freemen sell their crops, since the owner of that plantation is the only buyer). They will calibrate the entire system such that the freemen operate at permanent deficits – freemen’s cost of living exceeds income, such that they must borrow from the plantation owner every year to make ends meet. This is debt peonage, whereby the “freemen” are perpetually trapped in inescapable debt by design. The gentry doesn’t care about the principal that the freemen owe them – the amounts are completely arbitrary anyway, since they’re based on the very prices the gentry had set in the first place. The point is that the freemen are financially bound to the plantation, even while legalized slavery had been abolished.

For example, the terms the freemen face could include:

- $90 paid to the freemen for crops produced annually

- The gentry could then claim they’re only taking a paltry 10% cut of the crop sales!

- $40 charged for food and supplies

- $50 charged for rent

- $10 fee for transportation of crops to port

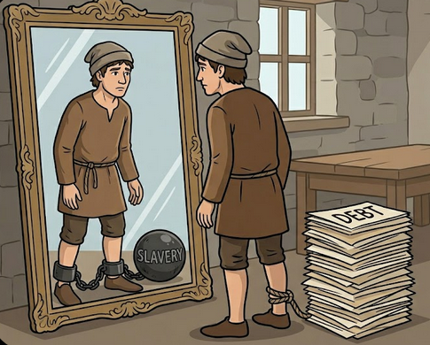

By design, the freeman is forced to borrow money from the gentry to make ends meet every year. As a result, their debt compounds. If, by some miracle, the freeman produced a profit one year, it would immediately be confiscated to offset outstanding loan balances.

Debt traps

There’s an entire world of difference between legitimate debt and debt traps. For the former, the lender actually wants to get paid back in full – they demonstrate the sincerity of their intent by running due diligence on the borrower, including analyzing debtor income relative to interest expenses and existing obligations, putting in covenants, assessing the value of collateral, looking at past track record (credit score or credit rating), etc. A successful loan for these creditors is when the loan matures with full repayment.

Do loan sharks, the mafia, or predatory credit cards look at these factors before offering a loan? Of course not – repayment of the loan in full is a bad outcome for them, as the entire point is to trap the borrower in perpetual debt. So long as the debtor cannot easily pay off the debt service costs and the debt balance accumulates with compound interest, they view it as a successful loan. Usurious debt (like offered by criminal organizations) serves as a pretext to extract surplus from the debtor – there’s no serious intent to recapture the “principal” on-time and in full.

The IMF is notorious as a debt trap for developing economies, and their heinous actions deserve their own article. Not only does the IMF exist purely to extract surpluses and keep economies constrained, they also serve geopolitical purposes for Western imperialism by forcing austerity (squeezing surplus) and privatization (selling off public assets to pay the loans), which opens the door for Western capital to acquire critical infrastructure assets of the nation for fire sale prices. Additionally, the IMF serves to bail out Western capital, most notoriously Argentina… The IMF doesn’t really take their underwriting seriously, as their debt sustainability analysis (DSA) is widely considered by experts as a total joke – it’s more a matter of geopolitics and elite interests rather than creditworthiness of the debtor country.

Let’s just call the freemen “serfs” from this point on, as that’s what they are.

Additionally, the gentry might push the government to pass laws that reinforce the dynamic, once again binding the labor to the plantation. For example, laws could make it illegal for serfs to be unemployed or for serfs to leave the plantation if they were in debt to the landlord. The elites would leverage the powers of the state to entrench themselves.

It should come as no surprise that little changed for newly freed black Americans living in the post-Civil War American South – despite their legal status changing on paper, the economic reality remained the same, because relative bargaining power didn’t change. Southern landowning elites used all of the aforementioned tactics, and then some. For black Americans, it took the collapse of Southern cotton and the massive labor demands of Northern factories during WWI to finally trigger a large-scale migration out of the South – most frequently to Chicago, Detroit, DC, Philadelphia, and NYC, following the railroad lines. The Northern capitalist elites immediately used these new arrivals as scabs to break strikes and work in some of the lowest paid and most dangerous and grueling factory jobs available.

Redistribution cannot permanently change surplus distribution

Suppose the government caps rent. As discussed before, the gentry would simply shift the extraction to another method, like increasing the cost of renting farming equipment. Relative bargaining power is unchanged and thus so is surplus distribution.

Suppose the government passes a redistribution law, whereby plantations are taxed at $10 annually per person they employ and then then paid out to each serf. In effect, the government has forcefully redistributed some surplus from the gentry to the serfs. However, this still has not fundamentally altered relative bargaining power between the two parties, and I think the reader knows what happens next: the gentry will simply readjust the terms of the serfs’ employment such that they recapture that $10, perhaps by increasing the cost of food sold at the plantations.

Suppose an international humanitarian group donates food to the serfs. What happens? The gentry immediately captures this windfall through perhaps a combination of higher rent and lower prices paid for the serfs’ crops. If the serfs are getting some free food, then the amount of resources they were previously expending on that food could be extracted. Relative bargaining power is unchanged and thus surplus distribution is unchanged – the humanitarian group should have just paid out the donations to the gentry directly and saved themselves the logistics expenses!

There is no incentive to innovate or pursue entrepreneurship

Highly asymmetric bargaining power ensures that the serfs will not be able to enjoy any surplus they can achieve through innovation or entrepreneurship. Again, the gentry can simply alter the terms of the deal such that the cost of living for the serfs (which the gentry sets) exceeds the value of the crops they grow (the price of which the gentry also sets). This ensures that all surplus flows to the gentry.

Suppose a serf develops a new technology that meaningfully improves yield per worker, such that the average serf could generate $130 worth of cash crops, compared to $100 previously. The only way for him/her to capture the value of the idea is to get patent protection, i.e. leverage the power of the state to enforce monopoly control thereon, which is probably since an agrarian economy would lack robust intellectual property protections to begin with. Similar to how Eli Whitney failed to capture meaningful profits from his cotton gin (and he was a white man), an innovative serf would fail to capture any value from his ingenuity. If the serf simply tries to share the technology with his fellow serfs so that they can overcome the debt traps, it’s only a matter of time before the gentry finds out and appropriates it, then increases extraction to capture all surplus created from the new technology.

In terms of entrepreneurship, how can that take place without capital, i.e. surplus? Even if there were capital for the entrepreneur, who would be his customers if nobody but the gentry has income to spend?

Additionally, there would be no education provided to the serfs anyways, since their only value to their employers is their labor. Education would only increase their bargaining power relative to the gentry, so there is absolutely no effort from the gentry or the government (again, likely captured by the gentry) to provide any form of education. Literacy might allow the serfs to read, understand, and negotiate their contracts – that can’t be allowed!

It’s clear that there is zero incentive to innovate or strive to create a better life when severely asymmetric bargaining power monopolizes all surplus in the system.

Only changes to RBP can structurally redistribute surplus

There’s only one solution: redistribution of critical resources – breaking the gentry’s control of the bottlenecks.

Notice that the source of the gentry’s bargaining power vs the serfs is their oligopoly control of key assets required by the serfs to make a living: the land, the tools, and the infrastructure (bringing food and supplies to the plantation). There is no competition whatsoever among the gentry for laborers (all gentry would lose if they compete), since their best interest is to collude.

The solution is land reform, aka land redistribution – breaking apart feudal estates and redistributing it to the farmers who tilled the land. There are several different ways to do it, but the main 2 ways historically were: 1) uncompensated land seizures (e.g. basically all communists) or 2) paying some lowball amount in government bonds (e.g. Jacobo Árbenz in Guatemala before being deposed by the US, post-WWII Japan) – the land then must be redistributed to the people or controlled by the state. The serfs had no money, so it’s not like they could have bought the land. Similarly, the state likely didn’t have much money anyways, since the economy is agrarian and underdeveloped. Frankly, the form of compensation rarely mattered; through redistribution, the landed gentry disappeared as a powerful political and economic force. Does it matter if someone is paid $0 for their land or $0.05 per acre for their land, as the government bonds issued in compensation rapidly became worthless due to inflation? The newly landed farmers didn’t care about inflation – they controlled real outputs of the economy, agriculture, so their crops simply increased in price. There also is no longer a “fair market value” for tenanted land, since the value of the land is based on the economics of the feudal system, which has since become unviable the millisecond the state indicated intent and capacity to crush it.

Land reform is one of the most powerful tools in the toolbox of reformers throughout humanity’s thousands of years of history, going all the way back to ancient Sumer under Uruk-Agina. It completely breaks the power of the landed gentry and has historically caused massive social upheaval, as the elite class frantically employs all means within their disposal to oppose such efforts.

Land reform as concessions to the people

Ironically, some of the most anti-communist forces in the world (US puppets) pursued land reform to stave off the growing influence of left-wing radicalism. Landed feudalism also stood as a barrier to industrialization, so it had to go for that reason as well.

Under American occupation led by Douglas MacArthur, Japan was forced to undergo extensive land reform, wherein huge chunks of land were sold dirt cheap to tenant farmers. By 1955, almost all tenant farmers disappeared. It is utterly ironic that MacArthur, one of the staunchest anti-communists during the Cold War, would implement one of the communists’ most radical policies.

South Korea (US puppet) bought up all tenanted land in 1949-1950 and sold to the farmers who tilled it. This was in anticipation of a North Korean invasion, as tenant farmers could easily be convinced to join the communists

In 1949, Taiwan’s KMT government (under US guidance) forced landowners to sell their land in exchange for industrial stock certificates. This was called “Land to the Tiller” reform.

South Vietnam (US puppet) launched a “Land to the Tiller” program in 1970s pushed entirely by the US. But it was too little too late. The Viet Cong offered the people land to make their living, while the South Vietnamese simply restored the landed gentry – it was obvious for whom the Vietnamese people were willing to fight.

American elites eagerly redistributed the lands of then Asian gentry, whose interests they didn’t care about, especially if it meant containing the influence of communists. This helped kick off rapid industrialization (“Asian Tigers”) and development. Western elites (the Epstein class) also own a ton of land in the West – they pivot wealth acquired elsewhere to park in massive landholdings. However, Western economies are already developed, so the people’s economic survival is not tied to land ownership (the French implemented land reform during the French Revolution).

Note that the Americans didn’t pursue land reform in the Philippines, another US puppet state (became independent in 1946). The Philippines didn’t need to be developed, as the US primarily wanted them to be an export colony for cheap agricultural commodities like sugar, hemp, and tobacco. Also, the Philippines was much farther away from the communist influence of China and the USSR than Taiwan, South Korea, and Japan. The country was better left in the hands of powerful local feudal elites, who took over large tracts of land previously owned by Spanish monastic landlords. That legacy of failure to implement land reform haunts the Philippines to this day. This has resulted in ambitious Filipinos forced to do migrant work abroad, as there simply aren’t enough economic opportunities domestically.

Then, all serf debt must also be cancelled to break the cycle of debt peonage – recall these were completely arbitrary loans anyways, fully designed to lock the laborers to the land. Again, this was a common remedy used throughout human history by reformers to break mass bondage and avoid civil unrest.

Sanctity of private property and contract rights

While the British and liberalism are known for their insistence on the sanctity of private property and contract rights, these ideas originated in ancient Rome, perhaps the polity where the elites were most powerful relative to the state (especially since the elites controlled the state). The Roman elites, intent on protecting their interests and huge bargaining power, codified the sanctity of private property, such that the private owner of the property has complete sovereignty over that property, such that the state or public has no say therein. The Roman concept of “dominium” conceptualized the idea of absolute ownership rights for property and land.

Unsurprisingly, the sanctity of contract rights also originated in ancient Rome, though the British and liberalism took it to a whole new level of near-religious zeal.

I hope it has become obvious to the reader the exact scenarios the inviolability of private property and contract rights were intended to prevent. If property rights are sacred, then the elites could never be deprived of ownership of critical chokepoints or assets to destroy their bargaining power advantage over the masses. In other words, land reform would be impossible. Additionally, the serfs technically agreed by contract to sell their labor to the gentry and eventually end up in inescapable debt, under the fear of starvation. The sanctity of contract rights also precluded the cancellation of unjust debt/contracts made between extremely unequal parties.

It doesn’t mean property rights or contracts shouldn’t be valid at all, but that people need to structurally analyze the implications of these policies when taken to extremes. I’m not here to push for a stateless, classless, moneyless society.

Additionally, the state must ensure no further bottlenecks exist, like tools, food, supplies, or transportation to market. Transportation can be publicly owned, and the other stuff can be managed by co-ops, whereby all of the new small farm owners have ownership stakes.

Once all this is achieved, the serfs have now become small landowning farmers who can keep most of the surplus for themselves. That said, remember that each farmer shouldn’t be individual bargaining entities – it would be much better if the farmers were to create a co-op merchant company that negotiates with foreign buyers of their cash crops on their behalf. Individual bargaining power is weak, but collective bargaining is strong. This is the best way to secure favorable prices in the global commodities market.

Of course, the gentry wouldn’t take kindly to any of these reforms and would aggressively oppose all efforts to undermine their control. There are no means the elites wouldn’t resort to in order to crush challengers, including intimidation, extortion, blackmail, or even assassination. They very well may go so far as to invite intervention from a neighboring plantation state, since the interests of elites are aligned. There is a well-documented history of plantation states suspending competition to send militaries to help each other crush slave rebellions (e.g. St. John rebellion, Berbice slave uprising), since those threaten their collective interests. Because they would never concede peacefully, the gentry must be liquidated or expelled from the country, the same way that the feudal Batista regime was deposed following the Cuban Revolution. This is not out of vengeance, but pure pragmatism.

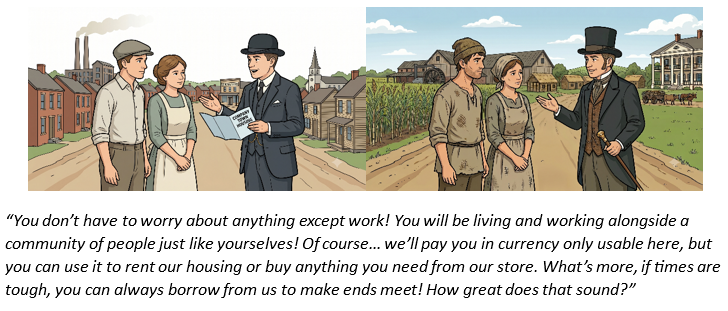

Company towns of the late 1800s and early 1900s

Would it surprise the reader to know that during this time, company towns that sprung up heavily resembled the feudal plantations I described earlier? The company controlled every aspect of the workers’ lives, reducing them to bare subsistence after their labor surpluses were extracted. Workers couldn’t really leave, and companies would provide all necessities, supposedly building utopian towns. Underneath all the propaganda was simply industrial age feudalism – the company held all the bargaining power and thus would endlessly extract surplus. All the mechanisms of extraction I discussed earlier, like debt peonage and scrips, were employed by these companies. They also controlled the flow of necessary goods like food and other household supplies, with a significant markup, of course. Going on strike or getting fired from one’s job in general meant losing shelter instantly, since the company owned all the housing.

Wrapping up 1.1

In this article, I’ve defined relative bargaining power and demonstrated how it impacts long-term surplus distribution.

- In Incumbency Theory 1.2, I will provide the most common sources of relative bargaining power and examples of how they’ve been leveraged historically to extract surplus from counterparties

- In Incumbency Theory 1.3, I will point out how liberal economic orthodoxy fails to contextualize its policies in the framework of relative bargaining power and thus fails to achieve the desired outcomes

However, with just the foundation of this article, I hope the reader has achieved a basic understanding of the relative bargaining power framework and can apply it broadly in their analysis.

Footnotes

- In the Nash Bargaining Solution, Nash referred to “walking away” point as “disagreement” point ↩︎

- There was a famous investment slide deck on Fiat Chrysler from 2015 that argued the auto industry was too competitive and too capital intensive, resulting in low returns for investors. The thesis argued for consolidation, i.e. significant M&A, within the auto industry to reduce costs and boost returns, the rationale being that there are too much duplicate R&D dollars spent across competitors. While that may be true, it leaves out a central driver of value for investors and loss for consumers: a lot less competition and spending on innovation. The evidence strongly supports this: decades of US protectionist policies going back to 1964 have insulated US automakers from healthy competition from foreign companies, resulting in lazy complacency in the domestic market. Consequently, US automakers have failed to keep up with foreign automakers, manifesting in receding market shares abroad. Protectionism has also hurt consumers via higher prices, lower quality, and fewer options. ↩︎